Section: New Results

Celer: a Fast Solver for the Lasso with Dual Extrapolation

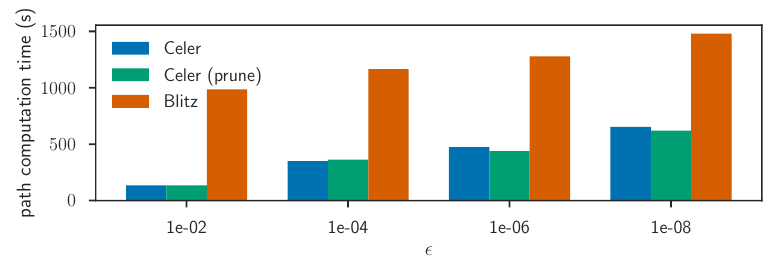

Convex sparsity-inducing regularizations are ubiquitous in high-dimensional machine learning, but solving the resulting optimization problems can be slow. To accelerate solvers, state-of-the-art approaches consist in reducing the size of the optimization problem at hand. In the context of regression, this can be achieved either by discarding irrelevant features (screening techniques) or by prioritizing features likely to be included in the support of the solution (working set techniques). Convex duality comes into play at several steps in these techniques. Here, we propose an extrapolation technique starting from a sequence of iterates in the dual that leads to the construction of improved dual points. This enables a tighter control of optimality as used in stopping criterion, as well as better screening performance of Gap Safe rules. Finally, we propose a working set strategy based on an aggressive use of Gap Safe screening rules. Thanks to our new dual point construction, we show significant computational speedups on multiple real-world problems compared to alternative state-of-the-art coordinate descent solvers.

|

More information can be found in [54]. Code can be found at https://mathurinm.github.io/celer/.